At the heart of being able to reach a much wider pool of businesses in need of financing lies cash flow based underwriting. In order to be able to make credit assessment without solely relying on often unavailable or dated financial statements, one needs to access alternative sources of data, bank transactions being one of the most dynamic and rich alternatives.

As traditional lenders grapple with outdated models, the tech sector offers SMEs a lifeline to growth and stability. In short, cash flow underwriting is revolutionary for VSB and SME.

This article explores the innovative methods supporting this shift and the impact on SME lending.

The evolution of underwriting

Underwriting is the foundation of the lending process, a method through which lenders assess the risk of lending money to applicants. Underwriting methods have evolved significantly over time, adapting to the changing landscapes of business and technology.

In the digital age, a third generation of underwriting has taken center stage: Data-Based Lending. This innovative approach uses advanced data granularity, leveraging real-time and tamper-proof data to make lending decisions. Data-Based Lending represents a medium-term investment strategy that balances high yield potential with medium risk, illustrating how digital transformation has enabled more dynamic and responsive financing solutions. This evolution reflects a broader trend towards utilizing data analytics and digital tools to enhance financial decision-making processes, offering a glimpse into the future of underwriting.

At Silvr, we have developed our own cash flow underwriting method leveraging open banking and bank statements data. This method incorporates real-time analytics to facilitate faster and more accurate credit assessment. This approach enables us to understand a business's current performance and potential, offering tailored financing solutions that traditional methods cannot match, thereby extending access to credit to as many businesses as possible, even those who would have been underserved elsewhere.

Key indicators for B2B credit assessment

Assessing an SME's health and viability involves looking beyond the surface level of financial statements, which are not always standardised or readily available. Adding to this complexity is the necessity to select the most suitable approach for each type of loan maturity. Whether it's short-term, mid-term, or long-term financing, each requires a tailored assessment, as they entail different risk considerations.

Bank Transactions: Silvr's key source of truth for short-term lending

When it comes to assessing SMEs credit potential, accessing recent financial statements is not always feasible. On top of this, Silvr recognizing the limitations of relying on extra financial sources like Amazon and Shopify connections—which often face issues such as lags, tracking problems and are not even utilised by the majority of SMEs—has focused on leveraging bank transactions analysis.

Thanks to the advent of Open Banking and Optical Character Recognition (OCR), Silvr capitalizes on the dynamic and timely data it provides. By collecting the last few months of bank transactions and utilizing bank statements if no Open Banking connection is available, Silvr transforms this information into digestible financial data through OCR technology. A variety of both positive and negative signals can be uncovered through bank transactions, in addition to running a more typical credit analysis. This system provides enhanced security by integrating anti-fraud mechanisms to ensure the integrity of this data.

Therefore, bank transactions emerge as a true source of factual and recent truth, offering a tangible foundation for making decisions on short-term lending. This approach not only avoids the inefficiencies of more traditional data sources but also aligns with the central beliefs of factual accuracy and recency, making it a genuinely actionable asset for credit assessment.

The Impact of Bank Transaction Analysis

Bank transaction analysis transforms raw financial data into actionable insights, providing a foundation for informed lending decisions.

Financial reconstruction

By offering a detailed view of cash flow, income, and expenses, bank transactions allow for a more accurate reconstruction of financial statements.

Risk evaluation

Patterns within transaction data can signal early warnings of financial distress or highlight areas of growth, informing risk management strategies.

Revenue and expense trends

Analyzing transactions helps us understand an SME's operational efficiency, spending habits, and overall financial health.

Business model viability

Transaction data may provide insight into the short-term sustainability of an SME's business model, potentially indicating its ability to generate consistent revenue.

Furthermore, by dynamically generating credit scores, Silvr proficiently adapts its pricing models to accurately assess the financial health and quality of companies within our acquisition funnel. This innovative approach not only simplifies the lending process but also ensures a dynamic response to the economic landscape, demonstrating how technology can enhance financial services.

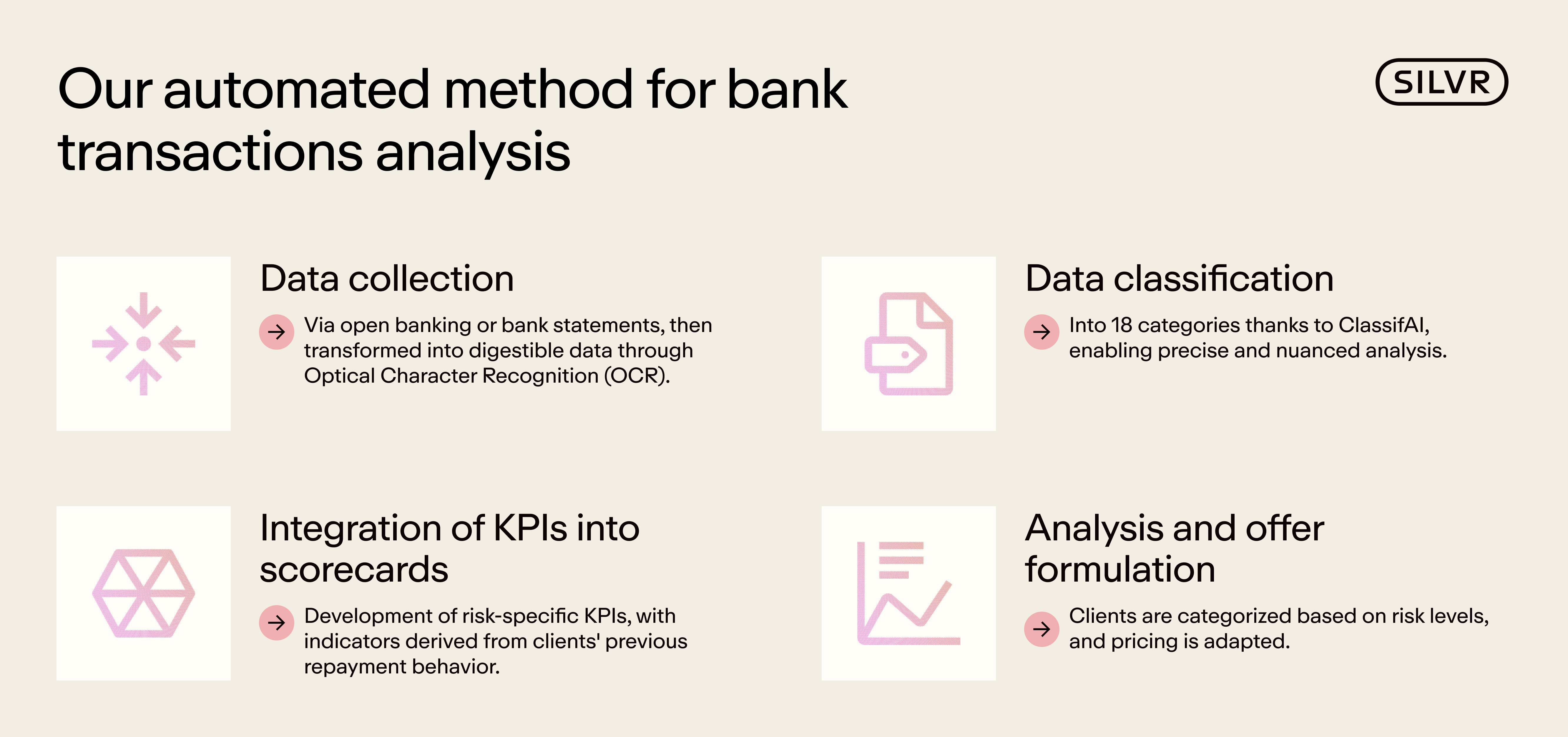

Analyzing banking transactions: Silvr’s automated approach

Thanks to cutting-edge automation tools and the technologic partnership we have with Google, Silvr's platform transforms the process of credit decision-making, automatically handling loans under a certain amount. Through an automated system, loan parameters including amount, duration, and commission are meticulously set to align with our internal IRR (Internal Rate of Return) objectives, ensuring a strategic balance between risk and return.

Data collection

The process begins with the retrieval of data via Open Banking or through bank statements, which undergo transformation through Optical Character Recognition (OCR), turning those into digestible data. Moreover, Silvr integrates sophisticated anti-fraud mechanisms to ensure the integrity and security of the financial analysis - but we won’t tell you the recipe obviously.

Data classification thanks to Silvr ClassifAI

The core of Silvr's methodology lies in its use of ClassifAI, an advanced machine learning tool that continuously improves by learning from the behavior of risk analysts and companies data. Through ClassifAI, data is classified into 18 transaction type categories, enabling precise and nuanced analysis.

Integration of KPIs into scorecards

It enables the creation of risk-specific KPIs, along with an added layer of indicators derived from clients' previous repayment behavior. These enhancements enrich Silvr's decision-making process and are integrated into credit scorecards.

Analysis and offer formulation

That enables swift credit decisions for loan issuance and categorizes potential clients based on their assessed risk levels. This strategic approach allows for pricing adaptation and assessment of the financial health and quality of companies within Silvr's acquisition funnel, showcasing a sophisticated, data-driven approach to SME lending.

Get to know more about our method in our article “Cash flow based underwriting supercharged by ClassifAI”

Conclusion

Capitalizing on its streamlined risk assessment method, Silvr is leading the way for SMEs to access timely financing, a domain traditionally monopolized by incumbent financial institutions and more traditional players. While these institutions rely on traditional analytical approaches to minimize their risk, Silvr's mission is to empower entrepreneurs by providing tailored support that aligns closely with SMEs’ needs.

By employing advanced AI technology and innovative products, Silvr has successfully tapped into the $5.2 trillion unmet market opportunity for SMEs¹ —a goal it aimed to achieve since day one. Its strong traction is already proven on mainstream SME customers.By leveraging insights from bank transactions, Silvr offers a swift and tailored response to its clients. Silvr stands as a testament to how technology and data analytics can transform the financial sector, offering more accessible and efficient financing options to SMEs, thereby fueling their development and contributing significantly to the broader economy.

¹ Small and Medium Enterprises (SMEs) Finance, The World of Bank, Oct 16, 2019

.jpg)